As proposed in the budget 2015, the statutory changes for MTD 2015 are as follows:

a. Income Tax For Resident Individual

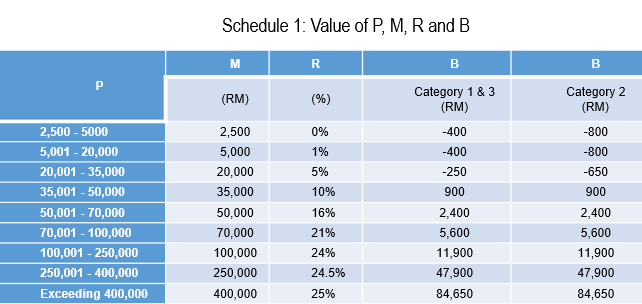

Therefore, the new tax rate value of P, M, R and B for MTD Computerised Calculation schedule 1 as follows:

b. Income Tax For Non-Resident Individual

Presently, a resident individual taxpayer is given a deduction up to RM5,000 for medical expenses incurred for treatment of serious diseases for the taxpayer, his/her spouse and his/her children.

As proposed in the 2015 Budget, the deduction for medical expenses incurred for serious disease be increased to RM6,000.

Presently, a resident individual taxpayer with disabled child as certified by the Department of Social Welfare is eligible for a deduction of RM5,000 for each disabled child.

As proposed in the 2015 Budget, the deduction be increased to RM6,000.

Presently, a resident individual taxpayer is given a deduction up to RM5,000 for the purchase of any necessary basic supporting equipment for the use of the disabled taxpayer, his/her spouse, children and parents.

As proposed in the 2015 Budget, the deduction be increased to RM6,000.